Wall Street hammered by bleak new economy reports

Go Deeper.

Create an account or log in to save stories.

Like this?

Thanks for liking this story! We have added it to a list of your favorite stories.

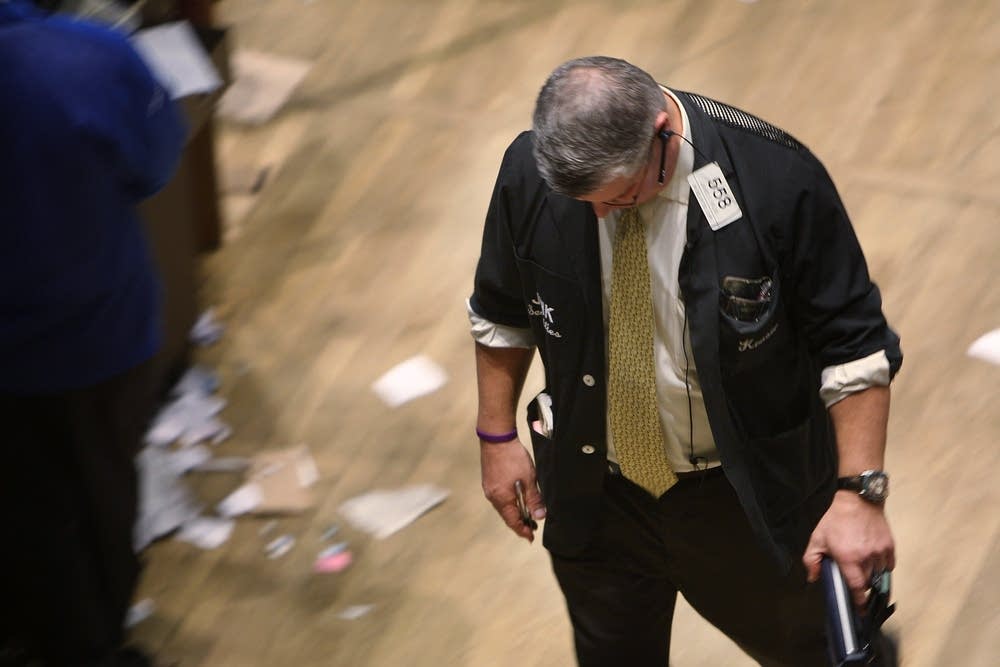

A fresh wave of bad economic news, including a half-million Americans newly out of work and the weakest October retail sales in nearly 40 years, pummeled the stock market Thursday, driving the Dow Jones industrials under 9,000 again with a stunning two-day decline of 10 percent.

The high market volatility that characterized the financial meltdown in September and October has returned, and the economic picture is growing notably bleaker, with both the holiday shopping season and the new administration of President-elect Obama looming in coming months.

Henry Paulson, President Bush's treasury secretary, pledged to work closely with Obama for a smooth handoff of power. Paulson said a "methodical and orderly" transition was in the best interests of the financial markets.

Those markets are rattled all over again. The Dow fell 443 points Thursday, on top of a 486-point drop on Wednesday. The 10 percent decline for the average is the worst over any two days since 1987.

Turn Up Your Support

MPR News helps you turn down the noise and build shared understanding. Turn up your support for this public resource and keep trusted journalism accessible to all.

Thursday's drop took the Dow to 8,696. It had just climbed back over 9,000 last week with its best week in 34 years.

The decline came with a heap of new economic indicators, all of them discouraging:

- The Labor Department reported 481,000 new filings for unemployment benefits for last week, slightly lower than the week

before but well into recession territory.

- The total number of people drawing jobless benefits in late October rose to 3.84 million, worse than analysts had expected and far higher than a year ago. The last time the figure was that high was February 1983, toward the end of a painful recession, although the work force then was only about two-thirds the size it is today. The increase in people on the rolls suggests the out-of-work are having a harder time finding jobs than in previous weeks.

- Retail sales for October were the worst in at least 39 years, according to the International Council of Shopping Centers-Goldman Sachs index, suggesting shoppers will be skittish this holiday season.

- Productivity of U.S. workers slowed dramatically in the summer, another Labor Department report showed. Labor costs rose.

- The International Monetary Fund, in an updated forecast, predicted the economies of the United States, Europe and Japan will shrink in 2009. If that proves correct, it would mark the first annual decline by such "advanced economies" since World War II.

- Target Corp. and Costco were among the many retailers reporting sales declines last month. Even teens stayed away from malls. American Eagle Outfitters Inc. and Abercrombie & Fitch Co. reported drops in sales. Cisco Systems issued a warning about slumping demand, sending shudders through technology companies. Auto parts maker Dana Holding Corp. said it will cut 2,000 more employees than originally planned after a bigger loss in the third quarter. Wal-Mart Stores Inc. managed a sales gain as shoppers hunted for bargains.

The government's monthly jobs report is due out Friday, and net job losses for October are expected to be about 200,000. The unemployment rate, now at 6.1 percent, is expected to rise to 6.3 percent. If it does, it would match the highest unemployment rate that was logged after the last recession, in 2001. The jobless rate hit 6.3 percent in June 2003 and then started to drift downward.

To provide fresh relief for economic troubles, House Speaker Nancy Pelosi said Democrats, in a lame-duck session later this month, would push to enact another stimulus package, possibly including extending jobless benefits beyond the usual 26 weeks.

Companies are begging for help, too. The leaders of General Motors, Ford and Chrysler and the president of the United Auto Workers union came to Capitol Hill to discuss billions of dollars more in financial help.

As the threat of a global recession grows, the European Central Bank cut interest rates by half a percentage point to 3.25 percent. And the Bank of England made an even more aggressive reduction, by a whopping 1.5 percentage point, its biggest in 27 years. Comments by the ECB president suggested the bank did not cut further because it was worried about triggering inflation.

The Federal Reserve ratcheted down interest rates to 1 percent last week and left the door open to further reductions in a bid to prevent a prolonged recession in the United States. The U.S. economy shrank slightly in the third quarter, its worst showing since 2001. And as jobs disappear, Americans will probably spend even less.

---

(Copyright 2008 by The Associated Press. All Rights Reserved.)

Dear reader,

Political debates with family or friends can get heated. But what if there was a way to handle them better?

You can learn how to have civil political conversations with our new e-book!

Download our free e-book, Talking Sense: Have Hard Political Conversations, Better, and learn how to talk without the tension.